2024 Market Outlook

Get exclusive market updates and the latest currency exchange news sent straight to your inbox

Insights from the dealing desk

16 minute read22 January 2024

2023 Overview

Looking back to January last year, the outlook was arguably bleak. The end of 2022 saw the post-COVID momentum grind almost to a halt and left many major global economies fearing recession in 2023. Markets anticipated that interest rates from the Bank of England, Federal Reserve and the European Central Bank would peak early last year at 4%, 5.5% and 3%, respectively.

In reality, we saw a different story unfold. While interest rates approached their peak tentatively in the second half of the year, they generally surpassed initial expectations - with the exception of the Federal Reserve. Despite this, central banks did not dismiss the possibility of future rate hikes.

Interest rates closed the year on:

- Bank of England: 5.25%

- Federal Reserve: 5.25 – 5.5 %

- European Central Bank: 4%

Inflation also deviated from its expected trajectory. Until at least last summer, central bank forecasts expected the 2% target to be reached only by 2025. However, across all three economic areas, inflation decelerated more than expected. Here’s how inflation changed in 2023:

| January 2023 | November 2023 | |

| United Kingdom | 10.1% | 3.9% |

| United States | 6.4% | 3.1% |

| European Union | 8.5% | 2.4% |

Data sourced from Bloomberg

At the end of last year, we began to see more of a divergence in inflation data and that had a significant effect on central bank policymakers’ decisions.

In December, the Federal Reserve held rates for the third consecutive month. The unanimous decision sparked a surge in stocks and bonds across the globe, and the Fed’s more dovish stance seemed to have a wide-reaching impact as markets increased their predictions for rate cuts in the US, UK and Europe next year.

The Bank of England and the European Central Bank also opted to hold rates steady in their last policy meetings of the year. Although the outcome was the same as the Federal Reserve the day before, the sentiment behind the decisions was markedly different.

Whereas the Fed’s market-moving comments from Jerome Powell suggested interest rate cuts were coming “into view”, his counterparts in Europe were more cautious. Their statements seemed to imply rate cuts were not yet on the agenda, with ECB President Christine Lagarde saying, “We should absolutely not lower our guard,” and Bank of England Governor Andrew Bailey reiterating monetary policy would remain restrictive for some time yet. What was perhaps even more insightful into the Bank of England’s stance was that three of the nine policymakers voted to raise rates again.

The aftermath was positive for sterling and the euro, which both posted gains following the central bank meetings.

Last year also saw a turbulent year in terms of geopolitical risk, with the Russia-Ukraine war continuing, and the Hamas-Israel conflict significantly increasing tensions in the Middle East. Both had effects on global financial markets which we will likely continue to see in 2024.

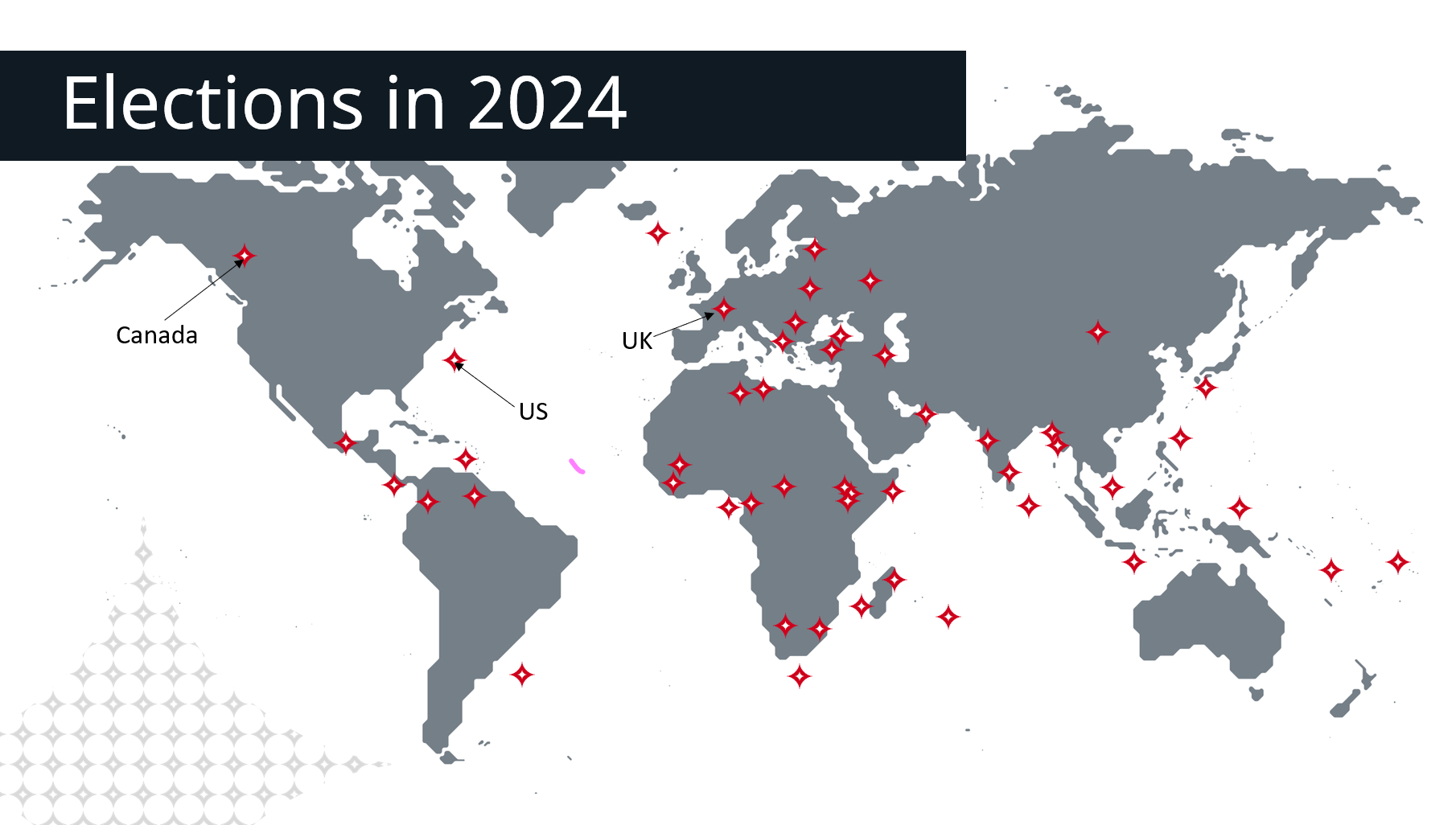

As we enter 2024, interest rates are expected to still be a primary driver of currency value. How currencies perform will likely be linked to how policymakers navigate the spectrum of inflation, growth, and interest rates over the next 12 months. At one end of the spectrum, economies could see inflation continue to decrease, growth data strengthen, and interest rates begin to come down. On the other end, inflation may remain too high or stagnate in its deceleration alongside stalling growth, which could mean central banks are left little choice but to leave interest rates higher for longer. Even the few initial data releases so far this year have begun painting opposing pictures for the UK, EU and the US. Last week, we saw EU inflation data indicate that it rebounded in December. Germany’s preliminary CPI data for the last month of the year came in at 3.7% YoY, 0.5% higher than the same metric in November. It was a similar story in France, where year-on-year inflation rose from 3.5% in November to 3.7% in December, and across the entire Eurozone, which saw the first inflationary increase in six months, rising from 2.4% in November to 2.9% in December. This was, however, 0.1% lower than the forecast from economists in a Reuters poll. US inflation also ticked higher in December, coming in at 3.4%, higher than the expected 3.2% and than the 3.1% reported for November. A higher-than-expected 216,000 jobs were added to the US job market according to data released by the Bureau of National Statistics on Friday 5th January too. The combination of importance and early release of the jobs data each month means it’s a vital economic metric for the Federal Reserve, giving it an indication of consumer spending. Both of these metrics coming in higher than expected could mean that the Fed will continue to tread cautiously, as a hot jobs market could fuel inflation. We also saw the minutes from the last rate meeting released earlier this month, which indicated that most Federal Reserve policymakers wanted to keep interest rates higher for longer, expecting only three-quarter point cuts in 2024. The UK, on the other hand, tentatively showed signs of decelerating inflation in early in 2024 before following the trend seen in the EU and US and recording a slight uptick in CPI inflation data. December’s inflation data was released on Wednesday 17th January showing an unexpected acceleration. The Consumer Price Index in the UK rose by 4% in December, up from 3.9% in November and 0.2% more than the 3.8% expected by markets. This is the first time inflation has risen since February 2023 and could relieve pressure on the Bank of England to start cutting rates. The major contributors to the increase were alcohol and tobacco after a recent increase in duty, which was balanced by the continued downward trend from food and non-alcoholic beverages. Earlier data seemed to support this, with research company Kantar published data on Wednesday 3rd January that showed grocery price inflation falling at the fastest pace on record in December, with annual inflation falling from 9.1% in November down to 6.7% in the run-up to Christmas. Figures released by the British Retail Consortium earlier in the week showed food price inflation also fall to 6.7% from 7.7% the previous month. While these declines can, for the most part, be attributed to Christmas promotions, with nearly a third of spending in the run-up to Christmas made on offer purchases, it represented the highest proportion of promotional spending since December 2020 and also the busiest Christmas for supermarkets since 2019. We could already be seeing a different narrative unfolding from the end of last year. Following the Fed’s rate meeting on 13th December, the Chair of the Federal Reserve, Jerome Powell, made market-moving comments which appeared to put the US on a faster trajectory to cutting interest rates, when compared to the more cautious words from the European Central Bank and the Bank of England following their final meetings of the year. The trajectory of interest rates throughout the year will likely be a key driver in currency performance. At the time of writing, markets are anticipating the following from the Fed, ECB, and BoE. Markets currently anticipate six rate cuts from the Fed in 2024, with current forecasts expecting the first cut in early May, although it could be as early as March. This would leave interest rates at 3.75% by the end of the year. In Europe, current projections have also priced in six rate cuts in this year. Forecasts expect the first will come in April or May with interest rates falling to 2.5% by the end of the year. Markets have priced four rate cuts from the Bank of England before 2025, slightly fewer than the other two central banks. They are also likely to start slightly later with a 75% chance of an interest rate cut in June and a 95% chance in August. We’re also about to experience a year that is jam-packed with general elections across the globe. The Financial Times has described 2024 as “the most intense and cacophonous 12 months of democracy the world has seen since the idea was minted more than 2,500 years ago.” To put this into perspective, this year will see about half of the global adult population (around 2 billion people) have the opportunity to vote. The most impactful could be the United States, which will see a Democrat candidate (likely the incumbent president Joe Biden) up against a Republican candidate, who is likely to be former president Donald Trump. Although many assume Trump and Biden will be the two leading political party candidates, they still need to be officially selected. This process kicked off on 15th January in Iowa, with Trump winning a landslide victory for the Republican candidacy, and will run until early March. While Donald Trump has been disqualified from running as a presidential candidate in the upcoming election in both Colorado and Maine - due to his involvement in the Capitol riot - these rulings are unlikely to have a substantial impact on his campaign. This is because, even without these disqualifications, he would have been unlikely to win those states anyway, given that Joe Biden won in both by a wide margin the 2020 election. Whatever happens, the next US election looks like it will be closely fought – national poll data in December had Trump on 44% of the vote and Biden trailing slightly with 42.6%. The UK is also expected to have a general election in Q3 of 2024. And at the moment, it’s looking more clear-cut on this side of the Atlantic. While the Conservatives will be hoping for their fifth consecutive victory after 14 years in power, the party’s popularity is trailing Labour’s significantly. An opinion poll from Ipsos in December showed a 17 points Labour lead, with 41% of 1,008 British adults asked, intending to vote for them. This compared to 24% for Conservatives. However, the Conservative government still have the Spring budget to come on the 6th March, before the new financial year starts in April, and there are rumours of another fiscal event before the election. Commentators and the press are currently speculating a host of tax cuts – potentially around inheritance and income tax – to be announced during the spring budget as the Conservatives try to hold onto power. China’s President Xi Jinping mentioned the country’s economic challenges when he rang in 2024 with his annual New Year’s Eve speech. He touched on the struggles of businesses and job seekers and the headwinds facing the country. The issues began when expectations of a roaring post-COVID bounce back instead saw cautious consumers saving their money, foreign investment pulling out, and serious problems befalling the property developers. This is significant because challenges in the property sector are felt more acutely in China, as up to 70% of the average household’s wealth is held in real estate. Last year also saw youth unemployment reach 21% in June before the government controversially stopped reporting on the figures. Now, the second largest economy could be looking at a complete restructuring of its economy – moving from a growth model to one more reliant on household consumption – in the hopes of avoiding stagnation of its growth. Policymakers will also have to consider China’s ageing and shrinking population alongside the historic challenge of reform in China. The Ukraine war and the conflict between Hamas and Israel are not showing any signs of coming to an end in 2024. Russia has increased its military spending, which could signal it’s preparing for a long war. Meanwhile, Ukraine’s prospects could be tied up with the US presidential election. The United States is the country’s most significant military supporter, with reports in December showing the Biden administration and the US Congress have contributed over $75 billion of aid. As much as 61% ($46.3 billion) has been military. Donald Trump, on the other hand, has previously stated that he could end the conflict in 24 hours by insisting the countries make a deal.There is also increasing scepticism among Republicans, culminating in the speaker of the House of Representatives, Mike Johnson, not agreeing to support Biden’s $61.4 million aid package in December. Israel has declared 2024 as the “year of war”, with Israeli defence officials and former senior intelligence officers expecting the fighting to continue for at least the next 12 months. The longer the fighting continues, the concerns around the conflict expanding into a wider Middle East war increase. Taiwan’s General Election also took place on Saturday, 13th January, with the landmark third term victory of the Democratic Progressive Party (DPP) having the potential to further inflame China-US relations. China had called it a ‘peace and war’ election and was accused of interference and trying to influence the voting population toward electing its preferred opposition candidate, Kuomintang (KMT). It has previously labelled the DPP as separatist. The US stated it did not have a preferred candidate. Either way, the outcome of elections in Taiwan may significantly impact the diplomatic relations between the United States and China because of Beijing’s continued assertion of sovereignty over Taiwan and the United States’s commitment to supporting Taiwan in its defence. Historically, although elections can impact volatility in the short term, they’re unlikely to have a significant long-term impact to the currency market. Overall, interest rates could remain a key driver in currency value in 2024. The trajectory for individual economies will depend on how central banks navigate inflation, growth, and their subsequent rate decisions. Already this year, we’re beginning to see more divergence from data releases which could indicate opposing economic pictures. The next monetary policy meetings are scheduled in late January and early February, and despite the probability of any change being low, markets will be closely monitoring the sentiment behind the decisions as they look for insights as to how they might play out across the rest of the year. Details on the next central bank meetings are as follows: Data sourced from Bloomberg This commentary does not constitute financial advice and all quoted rates are sourced from Bloomberg. 2024 Outlook

General Elections

China’s Economy

Geopolitical Risk

Central Bank Date Probability of Rate Cut European Central Bank Thursday 25th January 4% Federal Reserve Wednesday 31st January 5% Bank of England Thursday 1st January 5%

Author

- Joe Calnan, Corporate Dealing Manager

For more information on what our insights could mean for you call us on +44 (0) 207 823 7800 or open an account.

Whatever your payment needs are, we've got you covered

Regulatory info | Terms of use | Privacy Policy | Cookie Policy | Modern Slavery Act | Security | Open Banking | Sitemap

None of the information contained in this website constitutes, nor should be construed as financial advice.

Indicative rates are displayed on our website. We use interbank rates as a reference, and these rates should only be used as a guide.

Moneycorp is a trading name of TTT Moneycorp Limited, a company registered in England under registration number 738837. Its registered office address is at Floor 5, Zig Zag Building, 70 Victoria Street, London SW1E 6SQ and it is VAT registration number is 897 3934 54. TTT Moneycorp Limited is authorised by the Financial Conduct Authority under the Payment Service Regulation 2017 (firm reference number 308919) for the provision of payment services.

Moneycorp FRM is a trading name of Moneycorp Financial Risk Management Limited which is authorised and regulated by the Financial Conduct Authority for the provision of designated investment business (firm reference number 452443).

Travel money services are provided by Moneycorp CFX Limited. Moneycorp CFX limited is a company registered in England under registration number 4780562. It is registered office address is at Floor 5, Zig Zag Building , 70 Victoria Street, London, SW1E 6SQ and its VAT registration number is 897 393454.

Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated. Explorer™️ Card is issued by Prepay Technologies Ltd (PPS), with its registered office at Floor 6, 3 Sheldon Square, London W2 6HY UK. PPS is authorised and regulated by the UK Financial Conduct Authority for the issuance of e-money with firm reference number 900010.

© Copyright 2024 moneycorp